Life Insurance, often considered a crucial tool, provides financial security to policyholders and their families. Notably, Life Insurance policies are available in various types, catering to different needs and requirements of individuals. Understanding these policies’ features and rates is critical to making an informed decision.

Read ahead to learn about Life Insurance policy, their types and factors affecting their rates.

What are the Different Types of Life Insurance Policy?

Let’s read on to learn about the various types of Life Insurance policies available in the market:

- Term Insurance is a cost-effective plan that offers coverage for a period ranging from 10 years to 30 years. They tend to have lower premiums compared to permanent policies. Their premiums remain constant throughout the chosen term. Also, Term Insurance does not accumulate cash value.

- Whole Life Insurance offers permanent coverage and is valid for a lifetime. This insurance plan helps build cash value over time that can be accessed easily. Also, the premiums remain consistent during the policy term.

- Endowment plans offer a combination of both – savings and protection. Under this policy, the nominee gets the sum assured in case of the policyholder’s untimely death. Also, the policyholder gets a lump sum payout if he/she survives the policy term.

- Moneyback policies also help meet both the goals – savings and protection. But, the advantage is that a percentage of the sum assured is paid at a regular interval during the policy term.

- Variable Life Insurance offers death benefits to the beneficiary or family members of the policyholder. Also, this type of Life Insurance policy involves a cash value component and offers some flexibility in premium payments. Further, it allows policyholders to invest cash in various financial tools.

- Unit-linked Insurance plans, or ULIPs, offer a unique combination of insurance and investment.

Policyholders get to choose whether they want to invest in debt and equity. Also, there are no guaranteed returns, but a lump sum amount is received at maturity.

- Universal Life Insurance not only offers a death benefit but also features a savings component. Also, it comes with flexibility in premium payments and death benefit adjustments. Universal life insurance accumulates cash value over time.

- Children’s Insurance plans help to fund children’s education or marriage. One of the benefits of these plans is that children receive funds regularly. Parents buy these plans on their children’s behalf. They get a lump sum to cover their expenses in the absence of their parents.

- Annuity or Pension plans are specifically designed for retirement planning. These plans require policyholders to invest regularly for a predetermined period to receive regular income post-retirement. Also, these plans offer death benefits to nominees.

- Group insurance policies cover multiple individuals under one policy. Organisations buy these plans for their employees, offering benefits like health, life, and disability insurance.

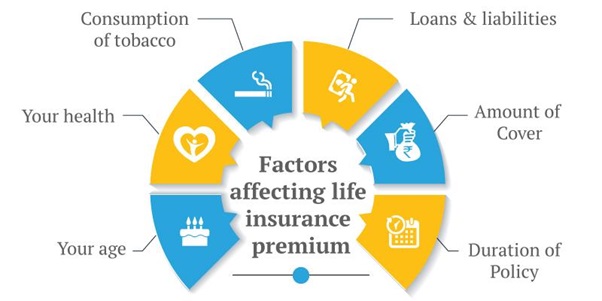

What Impacts Life Insurance Rates?

Here are the factors that affect Life Insurance rates:

- Life Insurance rates get impacted if lifelong coverage is included.

- Lower Life Insurance rates are available for younger individuals as they pose a reduced risk to insurance service providers.

- Individuals with pre-existing medical conditions or diseases face increased Life Insurance rates.

- Individuals who smoke or indulge in hazardous activities get higher Life Insurance rates.

- Family medical history can also influence the premium amount.

Final Words

Choosing the right Life Insurance policy involves carefully considering individual needs, financial goals, and preferences. Whether you need Term Insurance, Whole Life Insurance, Universal Life, or Variable Life Insurance, ACKO simplifies the process. As you explore options, ACKO ensures you have the information and tools (like the Term Insurance calculator) needed to make informed choices.

Follow this link to join our WhatsApp group: Join Now

Be Part of Quality Journalism |

Quality journalism takes a lot of time, money and hard work to produce and despite all the hardships we still do it. Our reporters and editors are working overtime in Kashmir and beyond to cover what you care about, break big stories, and expose injustices that can change lives. Today more people are reading Kashmir Observer than ever, but only a handful are paying while advertising revenues are falling fast. |

| ACT NOW |

| MONTHLY | Rs 100 |  |

| YEARLY | Rs 1000 | |

| LIFETIME | Rs 10000 | |